Singapore Mortgage Rates in 2026: Should You Fix or Float? (2026)

SORA is falling toward 1.32% by end-2026. If you're still on a 2023 peak-rate package, you could be overpaying $300–500/month. Here's how to check — and what to do before your next repricing.

You're coming up for mortgage repricing — and for the first time in three years, the question has flipped.

It's no longer "how do I survive rising rates." It's "rates are falling — am I on the right package, or am I leaving money on the table every month?"

Before you call your bank or sign that repricing letter, here are 3 things most Singapore homeowners never check:

- Whether their current rate is still competitive — banks quietly reprice existing customers worse than new ones

- Whether SORA or a fixed rate wins in 2026 — the answer depends on one number most people never calculate

- How much your actual monthly savings would be — and whether refinancing costs eat the gain

This guide covers all three. No banker jargon — just the mechanics and the 2026 data.

What Happened to Singapore Mortgage Rates Since 2022?

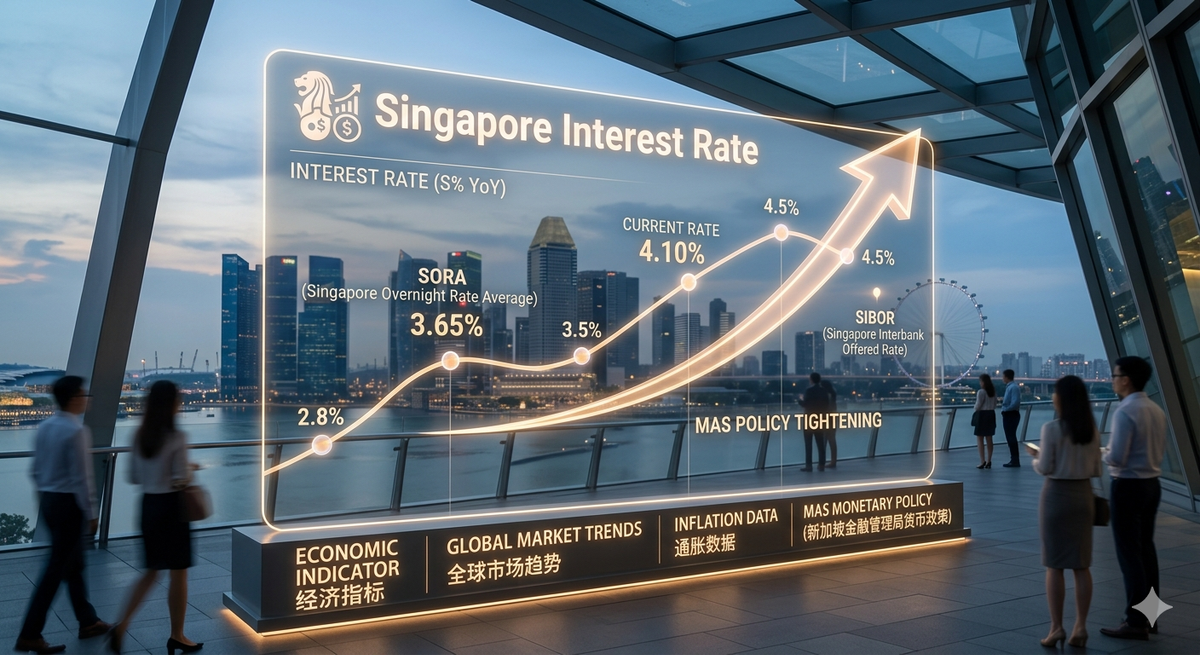

Singapore's home loan rates are anchored to SORA — the Singapore Overnight Rate Average — which replaced SIBOR as the benchmark in 2022. SORA tracks global rate cycles closely, particularly the US Federal Reserve.

From 2022 to late 2023, SORA climbed sharply as the Fed raised rates 11 times to fight inflation. Homeowners who took floating-rate packages in 2020 or 2021 saw their monthly payments jump significantly — in some cases, S$500–$800 more per month on a $1M loan.

The cycle has now turned. The Fed cut rates three times in 2025, and UOB Research (January 2026) forecasts SORA 3M to fall to 1.32% by end-2026, down from its peak above 3.7% in mid-2023. MAS has maintained a slightly hawkish stance on the SGD NEER, but domestic liquidity remains flush — deposits by foreigners have been rising even as SORA falls.

James's Note: Many clients I speak to are still on packages repriced at the 2023 peak rate. Some haven't checked in 18 months. In a falling rate environment, inertia costs you money. A 30-minute repricing review can save $300–500/month — that's $3,600–$6,000 a year on a typical $800K outstanding loan.

Fixed vs Floating in 2026: The Real Mechanics

Layer 1: How Fixed Rates Work in Singapore

Fixed rate packages lock your interest for 2–3 years. Banks price them based on their own cost of funds and where they expect rates to go — not where rates are today. In a falling rate environment, banks often widen the fixed-rate spread to protect their margins.

What this means for you: If SORA continues falling as UOB projects, a fixed rate locked today at 2.8–3.0% could end up more expensive than riding SORA down to 1.32% by end-2026 — by as much as 1.5% per annum.

Layer 2: How SORA Floating Packages Work

A typical SORA floating package is priced as: SORA 3M + spread (0.75%–1.00%)

If SORA 3M reaches 1.32% by end-2026 as projected, your effective rate would be approximately 2.07%–2.32% — meaningfully below most fixed packages available today.

Layer 3: The Refinancing Cost Equation

| Cost item | Typical amount |

|---|---|

| Legal fees (refinancing) | $1,800–$2,500 |

| Valuation fee | $500–$700 |

| Lock-in penalty (if applicable) | 1.5% of outstanding loan |

| Bank cashback (new package) | $2,000–$3,000 |

Break-even rule of thumb: If your monthly savings exceed $300, refinancing typically pays back within 12–18 months. If you're in lock-in, calculate whether the penalty eats more than 2 years of savings.

The Data Picture: Where Rates Are Headed

| Benchmark | Peak (2023) | Current (early 2026) | UOB Forecast (end-2026) |

|---|---|---|---|

| SORA 3M | ~3.7% | ~2.0% | 1.32% |

| SOFR (US) | ~5.3% | ~4.1% | 3.23% |

| Typical bank fixed (2yr) | ~3.8% | ~2.8–3.0% | — |

| Typical SORA float | ~4.5% | ~2.75–3.0% | ~2.07–2.32% |

Sources: UOB Global Economics & Markets Research, Jan 2026; MAS; individual bank rate cards

The SORA-SOFR spread — which widened unusually after April 2025's "Liberation Day" tariff shock — is now normalising. This supports the view that SORA has further room to fall even if the Fed holds steady.

The War Factor: How the Middle East Conflict Could Reshape Singapore Mortgage Rates

Just as the rate outlook was becoming clearer, a new variable entered the equation.

In late February and early March 2026, US and Israeli strikes on Iran triggered the largest energy supply disruption in recent history. Iran's closure of the Strait of Hormuz disrupted approximately 20% of global oil supplies, sending Brent crude surging over $110 per barrel within days. Wikipedia Brent crude prices jumped roughly 15% in the opening days of the conflict, then surged toward $120 a barrel as the market began pricing in the risk of sustained disruption. World Economic Forum

For Singapore homeowners tracking SORA, this matters — because oil prices feed directly into inflation, and inflation determines whether central banks cut, hold, or reverse course.

Scenario 1: Short Conflict — Rate Cut Path Intact

Most analysts believe the US military has the resources, capability, and will to prevent an extended closure of the Strait of Hormuz, and that disruptions will be measured in weeks rather than months. ICG In this base case, the energy shock is temporary, inflation stays contained, and the Fed continues its easing path. UOB's SORA forecast of 1.32% by end-2026 remains broadly on track.

For your mortgage: No action needed beyond your existing repricing review.

Scenario 2: Prolonged Conflict — Rate Cuts Delayed or Reversed

Sustained high oil prices could meaningfully delay monetary policy easing — and even though an oil price shock could also be seen as deflationary, the recent inflation period will prevent most central banks from reacting with monetary policy loosening. ING THINK

MAS already noted at its January 2026 policy meeting that ongoing geopolitical developments may push up imported costs TRADING ECONOMICS, lifting its 2026 inflation forecast to 1–2%. If oil stays elevated for 3–6 months, MAS may pause or slow its easing bias, keeping SORA higher for longer than UOB's base case projects.

A prolonged war that keeps energy prices high could drive up inflation and, with it, interest rates — piling pain on borrowers. CNN

For your mortgage: If you're repricing in Q2 or Q3 2026, the war scenario adds a genuine argument for locking in a fixed rate now — before banks widen their fixed-rate spreads further in response to inflation uncertainty.

What This Means for the Fix vs Float Decision

| Scenario | Probability (as of Mar 2026) | SORA outlook | Mortgage implication |

|---|---|---|---|

| Short conflict, quick resolution | Base case | Falls to ~1.32% by end-2026 | Float wins |

| Prolonged conflict, oil at $120+ | Elevated risk | SORA stays 2.0–2.5% through 2026 | Fix provides certainty |

| Severe escalation, Hormuz blocked | Tail risk | Rate cuts reversed, SORA rises | Fix becomes essential |

James's Note: I'm not in the business of predicting wars. But I am in the business of stress-testing your mortgage against scenarios that could genuinely hurt your cash flow. The war variable is real — and it's exactly why I run a 3-scenario analysis for every client before recommending fix or float right now. One number changes everything: where oil is in 90 days.

This section draws on: ING Think, March 2026; CNN Business, March 2026; World Economic Forum Global Risks Report 2026; MAS Monetary Policy Statement, January 2026; UOB Global Economics & Markets Research, January 2026.

✅ Reasons to Consider Floating in 2026 / ❌ Reasons to Lock Fixed

✅ You believe UOB's projection — SORA at 1.32% by end-2026 means floating could save you 0.7–1.5% annually vs fixed packages today. On an $800K loan, that's $5,600–$12,000 over two years.

✅ You have buffer — if your household income can absorb a 0.5% rate surprise without distress, floating gives you upside with manageable downside.

✅ You're selling in 2–3 years — no point paying a fixed premium for stability you don't need if you're exiting before lock-in ends.

❌ Your cash flow is tight — if a $200/month increase would genuinely stress your household, the certainty of fixed has real value. Sleep matters.

❌ You're a landlord and your rental yield is thin — if your net yield after mortgage is below 1.5%, any rate surprise eliminates your buffer. Fix and protect the margin.

❌ You're buying now at full TDSR — new buyers stretching to maximum Total Debt Servicing Ratio should lock in certainty for the first 2–3 years while building equity.

The 3 Questions to Ask Before Your Next Repricing

Question 1: What is my current effective rate — and how does it compare to today's best packages?

Get your latest loan statement and calculate: outstanding balance × current rate ÷ 12 = monthly interest. Then check the best available SORA package today. The gap tells you your opportunity cost.

Question 2: Am I in lock-in — and when does it end?

Most Singapore home loans have a 2–3 year lock-in from drawdown. Refinancing before this period incurs a penalty of typically 1.5% of outstanding loan. Know your date before making any move.

Question 3: What is my break-even timeline on refinancing costs?

Divide total refinancing costs (legal + valuation − cashback) by monthly savings. If it's under 18 months and you plan to hold the property, refinancing almost always wins.

Who Should Prioritise This Review?

Strong fit — act now:

- Homeowners repriced at 2022–2023 peak rates still on old packages

- Landlords with floating packages now on high spreads from legacy repricing

- Buyers with loans expiring lock-in in 2026 — your repricing window opens now

Weaker fit — monitor but don't rush:

- Buyers who locked fixed in late 2025 at competitive rates — you may already be positioned well

- HDB owners on concessionary HDB loan (2.6% flat) — this analysis applies to private bank loans, not HDB loans

Bottom Line: Inertia Is the Most Expensive Mortgage Decision

The rate cycle has turned. What punished you in 2022–2023 is now working in your favour — but only if you act. Banks will not call you to offer a better rate. The repricing letter they send defaults to their standard package, not their best one.

In 2026, the homeowners who win are the ones who run the numbers, know their lock-in dates, and negotiate from knowledge — not habit.

The reframe: your mortgage rate is not a fixed cost. It is a negotiable expense that you review every 2–3 years.Treat it like one.

Want to Know If You're on the Right Package Right Now?

Bring me your loan statement — I'll tell you exactly what you're overpaying.

I'm James Ong, CEA-licensed property consultant with PropNex (CEA Reg No. R008385F). I help Singapore homeowners and investors review their mortgage positioning as part of a broader property strategy — not just the transaction, but the full cost of holding.

📲 WhatsApp me at 91111173 — tell me your outstanding balance and current rate. I'll show you the gap and whether refinancing makes sense for your situation.

Sources: UOB Global Economics & Markets Research, Outlook 2026, January 2026 MAS Monetary Policy Statements, 2024–2025 CPF Board — HDB Concessionary Loan Rate, 2026 Bank rate cards: DBS, UOB, OCBC, January–March 2026

Disclaimer: James Ong | CEA Reg No. R008385F | PropNex Realty Pte Ltd. This article is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor before making any mortgage decisions.