Hougang Central Residences (2026): What the $1.5 Billion Land Bid Really Tells You

Singapore's most-watched 2026 launch sits above Hougang MRT and becomes a dual-line interchange by 2030. Here's what the land price tells you about where this project is headed — and who should buy.

You've probably seen the headlines. A $1.5 billion land bid. CapitaLand. UOL. Singapore's first major integrated development above an MRT interchange in the northeast. And a price tag — somewhere north of $2,500 psf — that will reset the floor for District 19 permanently.

But here's the question that actually matters: is Hougang Central Residences a legitimate buy at these prices, or are you paying a premium for hype?

Let me walk you through the numbers, the comparables, and what the land economics really say — then give you a direct verdict on who should buy and who should wait.

What Is Hougang Central Residences?

The mixed-use GLS site at Hougang Central closed with a top bid of approximately S$1.5 billion, or S$1,179 per square foot per plot ratio. Located directly above Hougang MRT station, the 99-year leasehold plot is zoned for both residential and commercial use. Once completed, the project is expected to yield roughly 835 private homes, alongside over 430,000 sq ft of retail space that could reshape Hougang's town centre. 99.co

Under the joint development structure, CICT will develop and own 100% of the commercial component. CapitaLand Development and UOL, in a 50:50 joint venture, will develop the residential component for sale. Aperia

The project has since been formally named Hougang Central Residences, comprising 835 units ranging from 1+study to 5-bedroom layouts, integrated with Hougang MRT. Hougangcentral-residences

Completion is targeted for around 2030 or 2031. EdgeProp.sg

The GLS Land Bid: Aggressive or Rational?

Before you can assess whether $2,500+ psf makes sense at launch, you need to understand what the developers paid for the land — and why they paid it.

The tender attracted three bids. The top bid was submitted by a consortium comprising CapitaLand Development, UOL, Singapore Land, and Kheng Leong, together with CapitaLand Integrated Commercial Trust, at S$1.5 billion or S$1,179 psf ppr. Sim Lian Group came in second at S$1.47 billion (S$1,155 psf ppr), while Frasers Property, Sekisui House, and Lum Chang jointly submitted S$1.4 billion (S$1,100 psf ppr). Stacked Homes

That 2% gap between the first and second bids isn't developer recklessness — it's a signal of shared conviction. Such pricing proximity suggests shared confidence among developers in the fundamentals of the site, including its transport integration, commercial component, and positioning as a future civic hub. 99.co

Was the bid too high? PropNex head of research Wong Siew Ying noted that the top bid is not overly bullish, as some recent purely residential GLS plots in the OCR without any commercial component have already crossed the S$1,300 psf ppr mark. Stacked Homes

When you strip out the commercial obligation — a 300,000 sq ft CICT-retained mall, a bus interchange, a town plaza — the residential-only land cost normalises significantly. The winning consortium wasn't just buying homes to sell. They were buying a civic-scale urban asset.

How Does It Compare to Other Mixed Developments?

This is where the analysis gets instructive. Here's where Hougang Central's $1,179 psf ppr sits against comparable integrated GLS benchmarks:

Tampines Avenue 11 (Parktown Residence): The site was awarded for $885 psf ppr in July 2023, and launched in February 2025 as Parktown Residence, with 1,041 units — 87% of total — sold at an average price of $2,360 psf over its launch weekend. EdgeProp.sg

Tampines Street 94 (Pinery Residences): Fetched $1,004 psf ppr in October 2024. 99.co

Chencharu Close: Awarded in September 2025 at $980 psf ppr. 99.co

Upper Serangoon Road (Stars of Kovan): Awarded at $845 psf ppr and developed into the 390-unit Stars of Kovan, completed in 2019. 99.co

The progression is unmistakable. Integrated development land rates in the OCR have risen from $885 psf ppr to $1,179 psf ppr in under three years — a 33% uplift in land cost alone. This has direct implications for what the next wave of new launches will cost buyers as supply tightens.

What Will Hougang Central Residences Launch At?

No official price list has been released. But the land economics give us a working range.

Based on the land rate of $1,179 psf ppr, analysts expect average selling prices in the $2,500–$2,600 psf range. Buyers are not just paying for location, but for convenience density, time savings, and long-term urban relevance. Plbinsights

The same consortium previously secured the Tampines Avenue 11 mixed-use site in 2023 and launched it as Parktown Residence in early 2025, achieving over 87% sales at an average price of approximately $2,360 psf during its launch weekend. The Hougang Central bid should therefore be viewed as an extension of a proven playbook, not an isolated gamble. Plbinsights

If Parktown Residence cleared $2,360 psf on an $885 psf ppr land cost, and Hougang Central's land is 33% more expensive, a $2,500–$2,600 psf launch is internally consistent — not inflated.

Why Integrated Developments Command a Premium — and Why It Persists

This is the part most buyers underestimate.

Integrated developments in Singapore have historically shown stronger price resilience and higher rental demand compared to standalone condominiums. Their integrated concept reduces reliance on cars and enhances daily living efficiency. Hougangcentralresidences

The Hougang Central structure goes a step further. With direct connectivity to the North-East Line and a planned link to the Cross Island Line by 2030, the site is poised to become a key transport node. Aperia You're not buying access to one MRT line — you're buying into a future interchange station. The MRT connectivity thesis here echoes what has driven value along the Upper Thomson corridor, where transit anchoring consistently underpins prices.

There's also an often-overlooked structural advantage in who owns the mall. Hougang Central's commercial podium will be 100% owned and managed by CICT — a professionally run REIT with strong incentives to keep the retail vibrant and well-tenanted. This is fundamentally different from strata-titled mixed developments where individual shop owners may leave units vacant for years and marketing budgets are difficult to coordinate. As someone who has managed residential estates from ECs to ultra-luxury condominiums, I've seen the difference this makes to estate quality, footfall sustainability, and long-term property values. From a property management standpoint, the CICT structure removes the most common failure mode of suburban integrated developments entirely.

Market watchers have noted that the retail component of Hougang Central could eventually be hived off into a commercial REIT. For a group that includes CapitaLand Integrated Commercial Trust, this optionality matters — residential sales are only one part of the total return equation. Plbinsights

The Demand Story: Why Hougang Is Ripe for a Reset

Hougang has not seen a new private residential launch since The Florence Residences in 2019. Over six years, demand has continued to build while supply has remained limited. When new supply finally enters a mature town after a long gap, pricing tends to reset — not because of hype, but because replacement cost has risen and buyers recalibrate expectations. Stacked Homes

HDB resale prices for four- and five-room flats in Hougang that are less than 20 years old have reached a median price of $675,000 and $830,000 respectively over the first 11 months of 2025. This price growth supports the pool of HDB upgraders in the area. Stacked Homes

Hougang ranks among Singapore's most populous precincts with nearly 230,000 residents, placing it in the top 10 of Singapore's 55 residential zones. Private retail space per capita in Hougang stands at 2.8 sq ft — significantly below the national average of 11.4 sq ft. Aperia

That retail deficit is important context. When a precinct is undersupplied on both private homes and quality retail, a single integrated project can reshape perceived desirability rapidly — the Sengkang Grand and Parktown Residence precedents both prove this.

ERA research notes this project is likely to attract both HDB upgraders and landed right-sizers, given it is Hougang's first private residential GLS plot in over a decade, since the Upper Serangoon Road site (now Stars of Kovan) was awarded in 2014. Era

James's Note: What Running Condominiums Teaches You About This Buy

Here's what most agents won't tell you when selling an integrated development.

The difference in running costs and resident experience between a professionally-managed, REIT-owned commercial podium and a strata-titled retail development is substantial and compounding. When CICT manages the mall, they bear vacancy risk, negotiate anchor tenants, and fund marketing from their own budget — not through levies on residents. The residential MCST is structurally ring-fenced from the commercial operations.

I've managed estates on both sides of this divide. The ones with professional commercial landlords on the podium maintain higher rental premiums, lower void rates, and better estate ambience over time. The ones with fragmented strata retail age poorly — and that deterioration shows in resale prices within a decade.

Understanding how home insurance and MCST obligations interact with your ownership structure matters too, particularly in integrated developments where the strata boundaries between commercial and residential are more complex. Before you buy, make sure you understand exactly what the management framework covers and where your liabilities begin.

ABSD and Financing: What Upgraders Need to Know

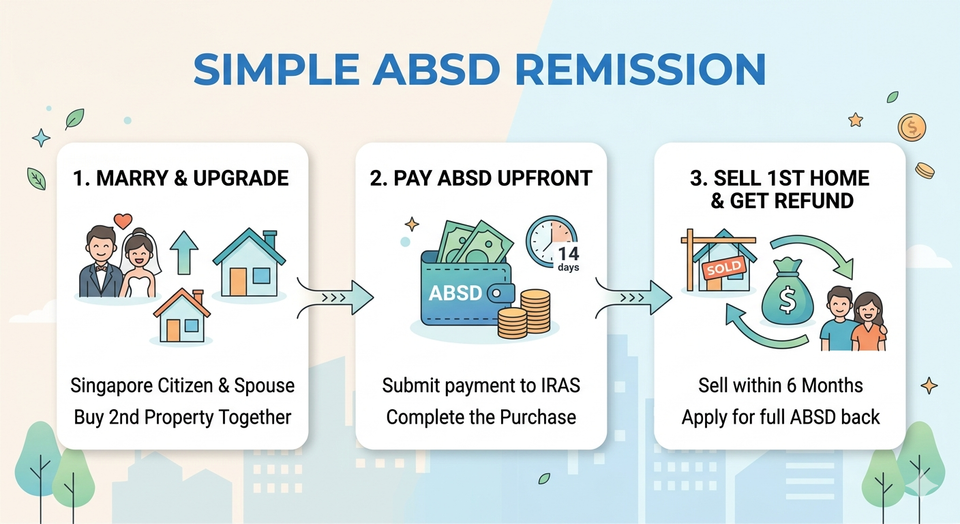

If you're an HDB owner upgrading to Hougang Central Residences as your only private purchase, you pay 0% ABSD on your first private property. But if you intend to retain your HDB while buying here, a 20% ABSD applies on the second property — a quantum that materially affects affordability at $2,500+ psf. Read the full breakdown of how ABSD affects your purchase decision before committing.

The TDSR headroom calculation is equally important. At an expected entry of $1.3–1.5 million for a 2-bedroom unit, your monthly debt obligations need to stay within 55% of gross income. Run the numbers honestly before the launch queue.

Who Should Buy Hougang Central Residences?

Strong buy for:

- HDB upgraders in Hougang, Kovan, Sengkang, and Punggol targeting their first private property — pent-up demand here is six years deep

- Investors seeking integrated development rental premium with a Cross Island Line interchange kicker from 2030

- Families prioritising MRT access, school proximity, and daily convenience in one address

Consider carefully if:

- You're comparing against resale condos at $1,400–$1,700 psf in the same postcode — understand you're buying a structurally different product, not just a newer one

- Your TDSR is tight at the expected quantum — size your unit to your financing headroom first

Timing note: Integrated MRT developments in OCR locations are moving into a higher pricing band. Future launches in mature estates are unlikely to be priced below today's benchmarks. Buyers considering large-scale, transport-linked projects may see fewer comparable options in the near term. Springleafcollection

Waiting for a correction here is a bet against six years of pent-up demand, a Cross Island Line interchange, and Singapore's most proven developer duo in the integrated development space.

Verdict

Hougang Central Residences is not a cheap buy. At $2,500–$2,600 psf, it will be the highest-priced private residential launch in Hougang's history. That is by design — the land economics, the development scale, and the CICT commercial structure all point there.

Hougang Central will likely serve as a pricing anchor for future developments in the area, much like earlier integrated projects did in other regional centres. Plbinsights

For buyers with a 10-year horizon — own stay or investment — the Cross Island Line integration by 2030, the professionally managed retail podium, and Hougang's deep HDB upgrader pool make this a conviction buy at the right unit, stack, and TDSR headroom.

Get the floor plans early. Projects of this nature do not give second-launch discounts.

Thinking about Hougang Central Residences? I'll walk you through the unit mix, stack analysis, and whether your HDB equity gets you to the right entry quantum — without the pressure.

📲 WhatsApp James at wa.me/6591111173

Sources: CapitaLand/CICT Press Release (Jan 2026) · 99.co · ERA Singapore Research · StackedHomes · PropertyLimBrothers · EdgeProp · PropNex Research (Wong Siew Ying)

James Ong | CEA Reg No. R008385F | PropNex Realty Pte Ltd This article is for informational and educational purposes only and does not constitute financial or investment advice.